Let’s establish three facts up front. One, the volume of contracts traded was not “millions” (as at least one conspiracy theorist is claiming). During the 1-minute window when the price of gold dropped from $1,254.10 to a low of $1,236.50 and recovered to $1,247, 18,031 August gold contracts traded. There was negligible volume in the October and December contracts.

Two, the Earth is round. This did not occur while “everyone” was sleeping (as at least one conspiracy theorist asserted). It happened when Europe was open and the UK had come online, at 9:01am British Summer Time (BST). China and Singapore were also open for business at that time.

Three, there was no single large futures trade that “smashed” the price but a large number of smaller trades, with the largest trade being 296 contracts (close to 1 ton or $36 million). The chart below shows milliseconds (1/1000th of a second) from 9:01:00 to 9:01:30 – 30 seconds.

![]()

At this timescale a lot of the trading is computer to computer, a fight between algorithms. We say fight, because the trading wasn’t entirely one way. Some time slots show upticks in price.

So what did happen?

We do not believe that one should try to look at whether spot or futures moved first, to determine which one is the driver of a price move. The timing is very close, due to high-speed fiber optic lines connecting market makers’ servers. And errors in timing, especially of a third party observing from the outside, could be greater than the timing of the events being measured.

We have a better way to answer this question. If the price of spot is falling relative to futures, then we know there was selling of spot. If the price of futures is falling relative to spot, then we know there was selling of futures.

This spread, future price – spot price, is called the basis.

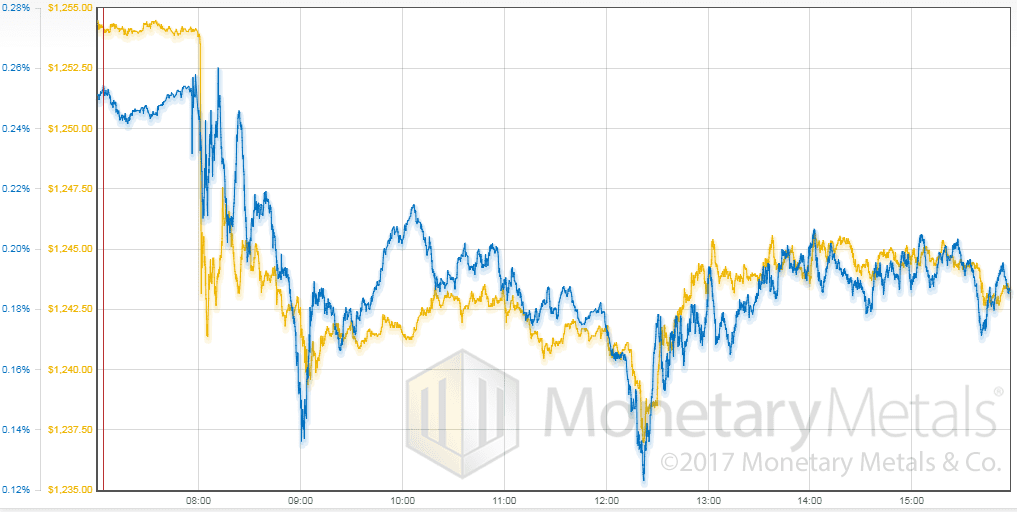

Here is a chart of the gold price overlaid with the August gold basis, showing the London trading day (times are GMT, so the chart beginning at 7am is really 8am as the UK is on daylight savings right now). The crash occurred at 8:01AM GMT, which is 9:01 BST.

We see a clear picture: as the price falls, so does the basis. This move was led by selling of futures. No, not a massive conspiracy. Indeed not massive at all.

And it should be noted that the basis did not move all that much. 10 bps. This suggests that though the move may have been driven by futures, there was plenty of selling of metal too.

Of course, if people were buying metal even holding the price constant while some nefarious party was selling futures, such that futures went down by $14, there would be nearly a $14 backwardation in the August contract. That is over 1%, or about 6% annualized.

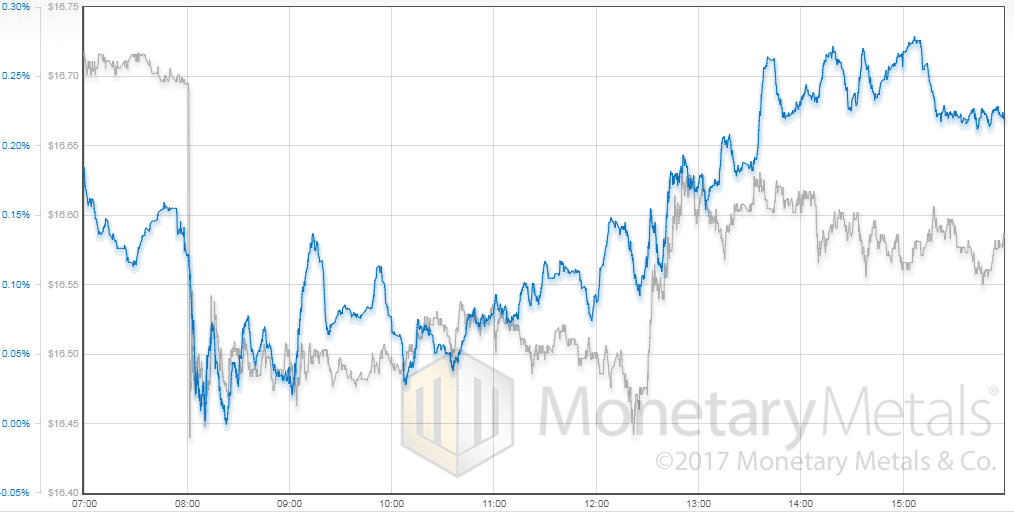

Now let’s look at the silver price along with the September silver basis, which behaved differently.

A 25-cent drop in price and a 15 bps drop in the basis also seem moderate. Futures sold off a bit, but the selling was by no means exclusive to paper.

And then, an hour later, look at the basis action. Someone—or many someones—is bidding up paper. Buying the dip. However, that had no impact on price, so there was also selling of metal. An hour after the buying began, it subsided. But then began anew. And for the next 5 hours, we see sufficient buying of silver paper, that the basis is pushed up above where it had started even though price peaked below the start and then subsided another nickel.

This is what it looks like when exuberance in the futures market meets selling of physical metal. Especially from around 13:30 GMT.

We call ‘em like we see ‘em.

Monetary Metals will be exhibiting and FreedomFest in Las Vegas in July. If you are an investor and would like a meeting there, please click here.

© 2017 Monetary Metals

0 comments:

Post a Comment